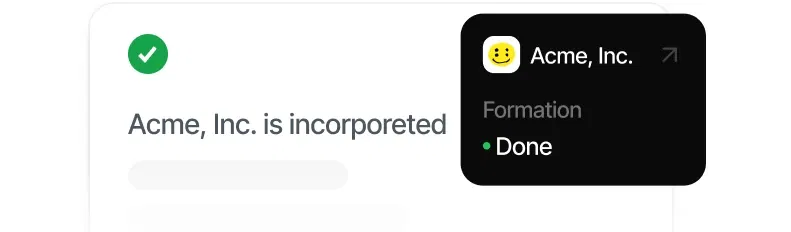

Formation

Form your LLC or C-Corp online.

We seamlessly handle your U.S. Formation, Business Banking and Compliance providing Every Solution you need to grow.

Get StartedWith Clemta, embark on a seamless business journey;

Form your LLC or C-Corp online.

Get expert help for your tax IDs.

Easy account setup with a debit card.

Keep your finances in check.

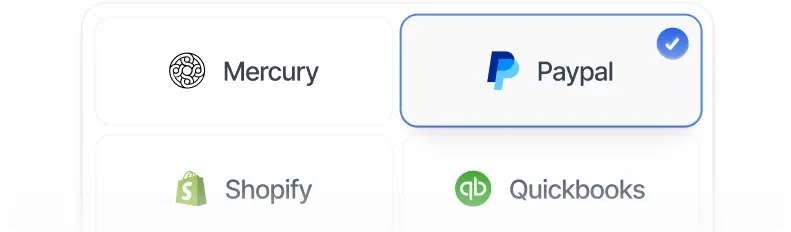

Integrate your stack with accounting features.

Simplify your tax filings with automated flows.

Once your business is up and running, our powerful dashboard will help you manage every aspect of your business!

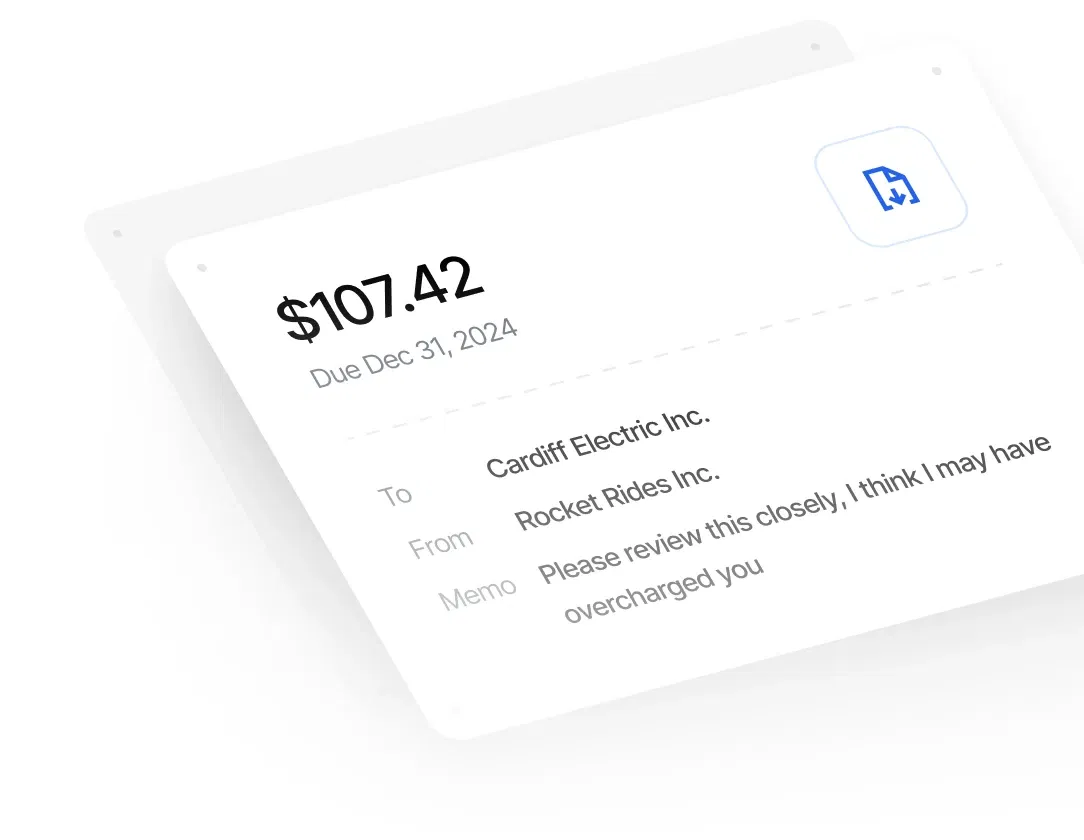

Create, send, and track professional invoices with just a few clicks.

Stay compliant and simplify tax preparation with our automated tax calculation and filing tools.

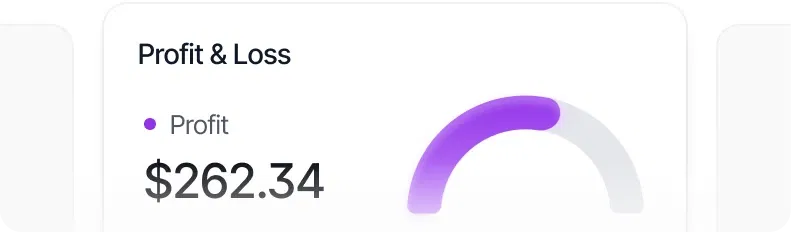

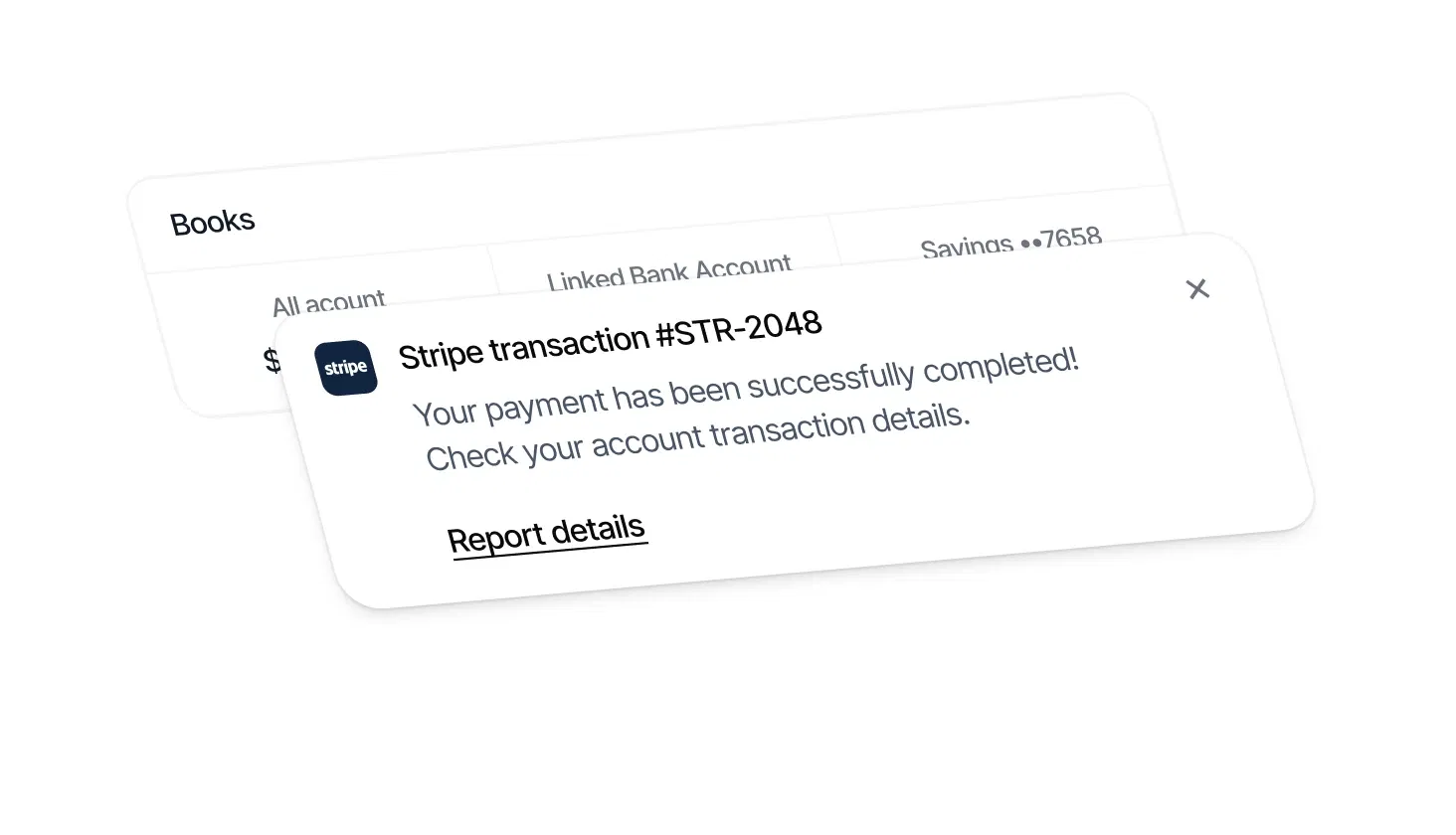

Keep your finances in order with our advanced bookkeeping features, including expense tracking, income recording, and financial reports.

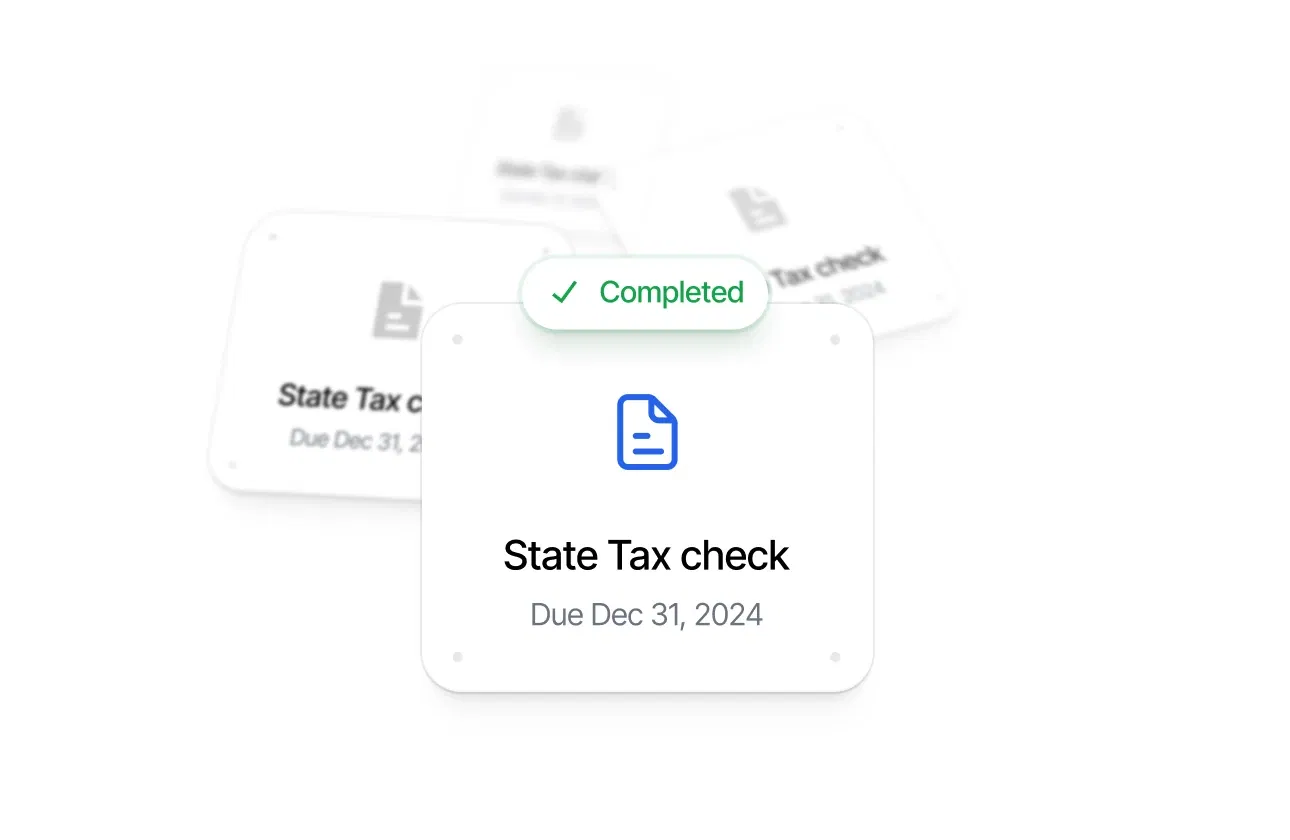

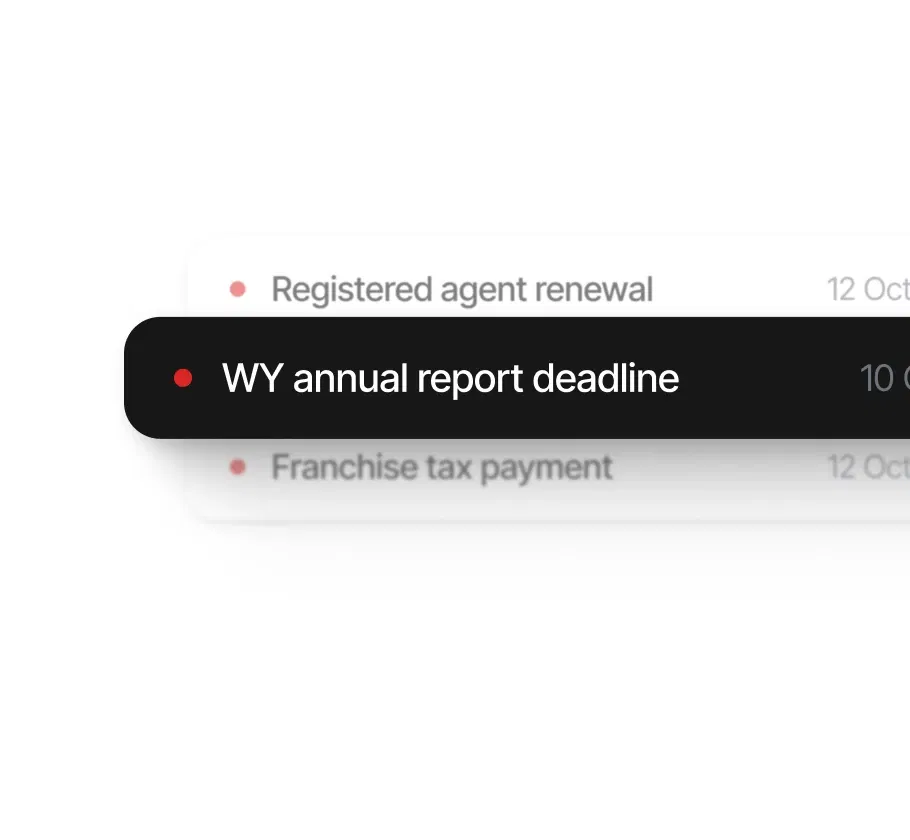

Track important deadlines, receive reminder notifications, and ensure your business remains compliant at all times.

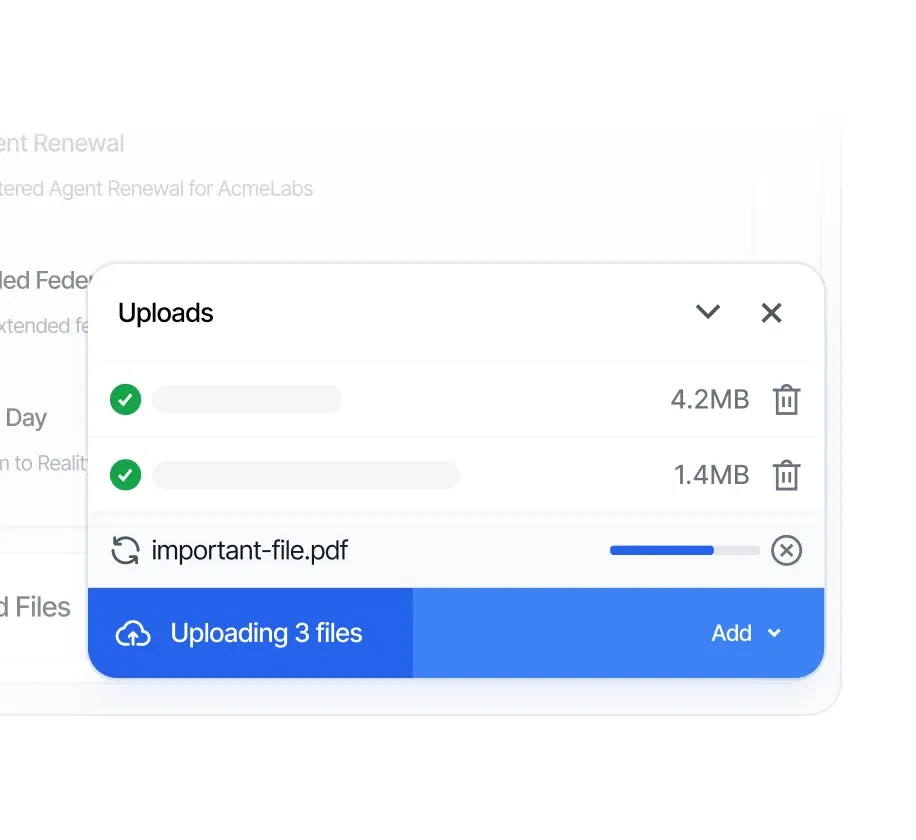

Find, review, and manage your files with ease, both on your desktop and mobile devices.

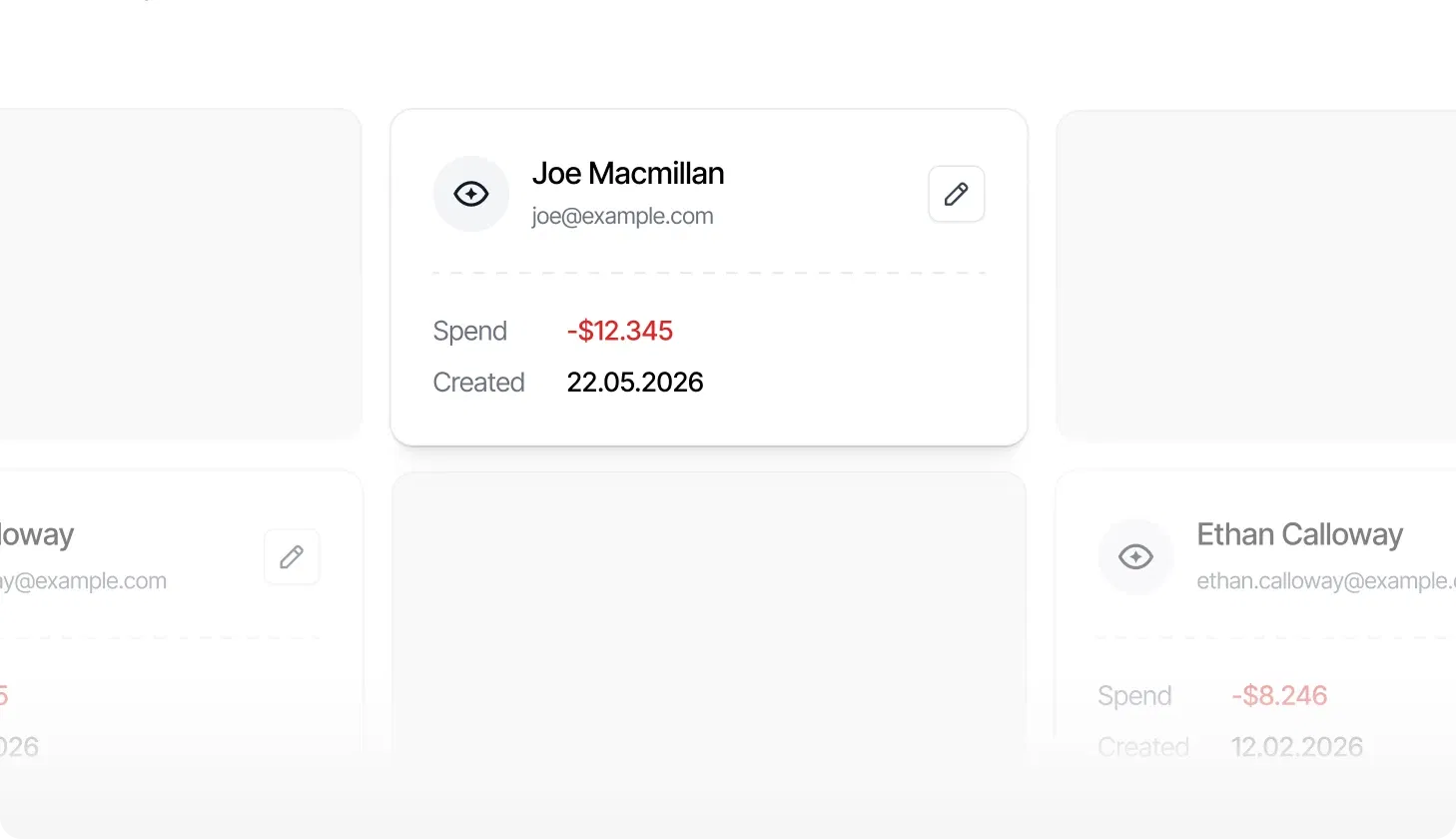

Organize and manage your clients' information with a user-friendly interface.

Special Offers

Special OffersBy joining our family, you will unlock exclusive perks worth $1,000,000+ from leading software and service providers!

Already incorporated? You can boost your business with our additional services!

Form your LLC or C-Corp online in minutes with our guided process.

Get your Employer Identification Number quickly and hassle-free.

Timely email reminders so you never miss a state or federal compliance deadline.

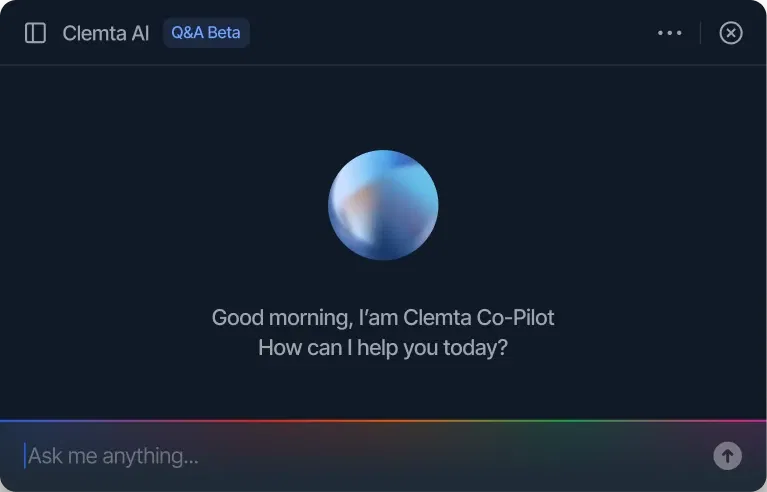

Clemta Intelligence makes running a US business simpler, smarter, and more accessible for founders everywhere.

Clear answers from your finances and compliance status.

Invoices, documents, and workflows with a single prompt.

Categorize transactions, reconcile accounts, check tax readiness, and keep your books current - just by asking.

Read success stories from small business owners to enterprises! Visit our clients' experiences below and discover how Clemta can help you turn your dream business into reality.

I have always received an immediate response. The quick response time from Clemta has truly made a difference in my interactions with the company. From assistance with company formation to the seamless process of opening a bank account, my overall experience has been great. Clemta's dedication to efficient and responsive service has truly stood out to me.

Talal Ahmed Raza

Fashion Retailer

Paul M.

Small Business Owner

I had a tax penalty due to unfinished post incorporation process & income taxes. Clemta helped me to get my 83b form submitted and finish my post incorporation. Now with almost $400 I saved almost $10k in such a short time.

Amr Maged

Amazon FBA

Clemta is excellent. All responses to my emails were quick, professional and to the point. When I needed arabic speaker to explain my query in deep, i immedialely got very good candidate.

Fatih Kadir Akın

Creator

Clemta was very supportive during the establishment process of the US company I set up for my e-books. They have organized every step so well that you're left with no question marks in your mind. They deserve every user and more!

Sultan Al Suwaidi

Ecommerce Founder

I recently used Clemta to set up my business in the United States, and I was very impressed with the service. The process was smooth and easy, and the customer support team was very helpful and responsive.